How 2 EU Aerospace Founders Secured Bridge Funding in 63 Days, Engaging 28 Investors

A case study in aerospace and dual-use bridge financing, cross-border investor targeting, national security and industrial resilience investing, and speed to close.

Overview

Founder Stage & Sector | Aerospace, Delivery Systems |

Core Offering | The first fully reusable small rocket platform utilizing proprietary, third-party validated propulsion technology that extends engine lifespan by 100x, with novel applications across commercial launch and dual-use defense markets. |

Engagement term | Q4 2025 |

Period of Performance | 2 Months |

Focus Area | Capital Raise, Advisory, Investor Relations |

Challenge

The founders entered venture capital conversations with a highly de-risked profile, anchored by strong commercial traction including multiple booked launches and multi-million-dollar annualized signed LOIs. Their first-mover advantage in fully reusable small-lift launch systems, powered by TRL7-validated propulsion technology with 100x engine life extension, set them apart from the competitive field.

This technological edge attracted institutional backing from leading European space agencies, a top-tier U.S.-based space accelerator, and a Canadian accelerator guided by aerospace industry pioneers. The venture also drew dual-use defense interest from military R&D institutions exploring hypersonic applications including ramjet and scramjet platforms.

Despite these strengths, three critical gaps were blocking the bridge round:

No hyper-targeted outbound capital-raising strategy to bypass traditional VC funnels, which were misaligned with the stage and structure of this opportunity.

Limited access to the right investor profile for a bridge of this structure: HNWIs, solo angels, and family offices capable of agile, sub-six-figure decisions.

The need to demonstrate a clear de-risking milestone to institutional investors, which required closing this bridge round first.

Execution was further compounded by limited founder bandwidth, a network already exhausted after conversations with 150+ investors, and geographic distance that reduced the viability of warm introductions. The short runway required rapid narrative repositioning. Early-stage aerospace hardware also carries higher investor skepticism than software-native plays given longer development cycles and capital-intensive milestones. Complex deep-tech concepts including electromethane fuel systems, TRL7 propulsion, and dual-use hypersonic applications required translation into a clear, commercially anchored investment thesis that non-technical angel investors could evaluate and act on quickly.

To overcome an exhausted network of 150+ investors, limited runway, and persistent skepticism toward early-stage aerospace hardware, SCG executed a hyper-targeted capital raise sprint that repositioned complex deep-tech capabilities into a clear, high-conviction bridge opportunity for HNWIs and family offices, bypassing traditional VC bottlenecks and unlocking the critical milestones required to support a credible Series A.

Advisory and Narrative Repositioning: SCG translated complex aerospace engineering into a commercially driven, investor-ready narrative aligned with buy-side expectations. The core outcome was reframing the bridge round as the direct catalyst for achieving a critical engine chamber firing milestone. By converting deep-tech complexity into a clear, investable thesis, SCG enabled non-technical angels and HNWIs to quickly grasp the scale of the opportunity and overcome traditional hesitation around aerospace CAPEX and long development cycles.

Capital Raise Sprint Execution: Operating beyond an exhausted pipeline of 150+ previously contacted VCs and across geographic constraints, SCG rebuilt the investor pipeline from the ground up. This included leveraging proprietary investor networks and sourcing new, thesis-aligned prospects specifically targeting early-stage aerospace opportunities. The strategy prioritized high-conviction capital sources: solo angels, angel networks, and family offices, which comprised approximately 67% of the engaged pipeline, optimizing for speed, flexibility, and bridge round execution.

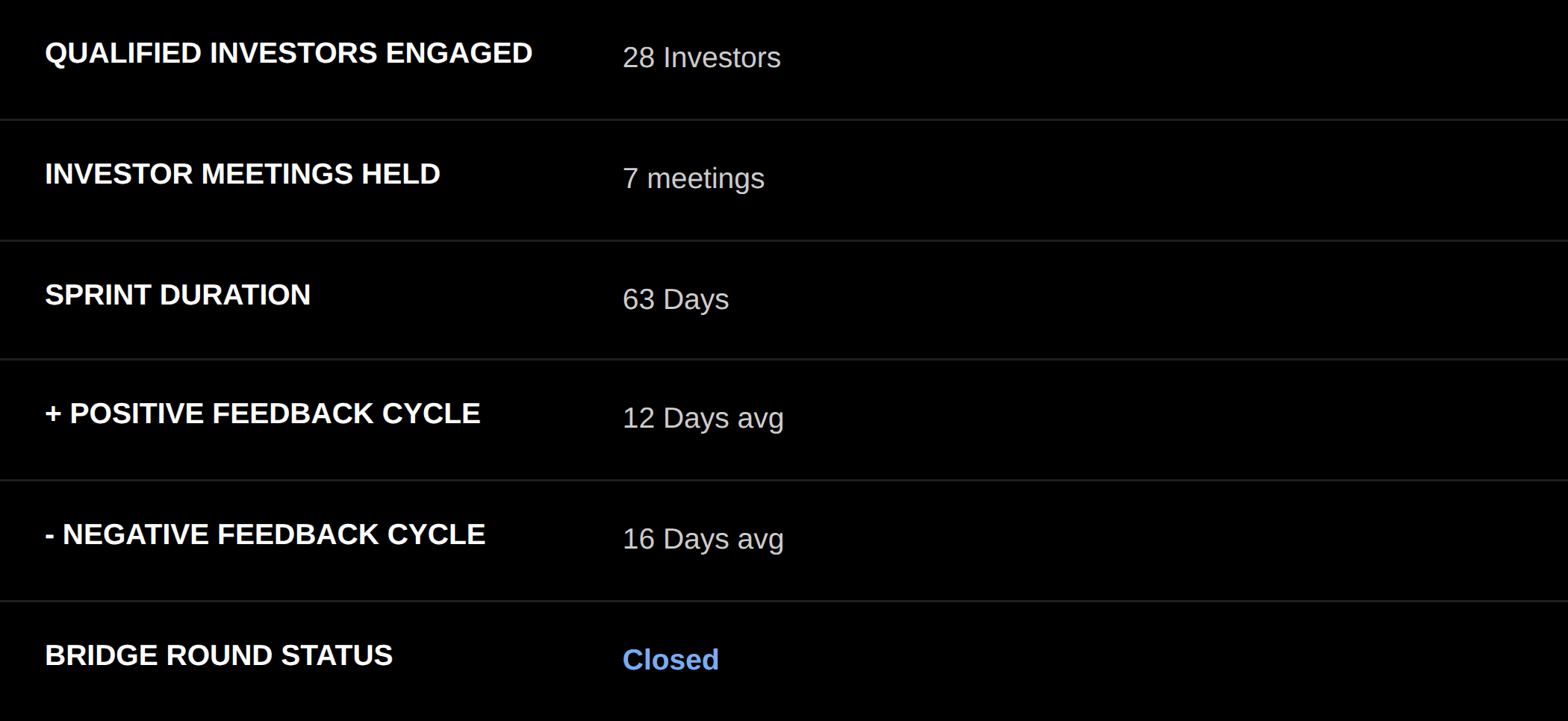

U.S. Investor Relations and Pipeline Management: SCG led end-to-end investor relations and pipeline execution with a focus on speed, engagement, and conversion. Using behavioral data insights including identifying Fridays as the highest-converting response window, the team deployed up to four highly targeted follow-ups per prospect to drive decisive outcomes. This disciplined approach generated engagement from 28 qualified investors, secured high-value meetings, and captured critical market intelligence on institutional thresholds, directly informing the company's Series A positioning.

The engagement reactivated investor momentum across a previously exhausted pipeline, engaging 28 qualified investors and securing high-value meetings while anchoring the bridge round around a critical de-risking milestone. The bridge round was successfully closed, enabling the founders to advance toward that milestone and enter Series A conversations from a position of strength.

This engagement illustrates a challenge common to deep-tech founders at the pre-Series A stage: strong fundamentals undermined by audience-strategy mismatch. The company was not lacking commercial traction. The core issue was structural: a pre-revenue, hardware-centric bridge round was being pitched to later-stage institutional VCs operating with software-like expectations, requiring $2M+ ARR or a completed technical milestone before committing.

Compounded by an exhausted network of 150+ passed investors, limited founder bandwidth, and persistent skepticism toward long-horizon aerospace CAPEX, the company was effectively locked out of its own pipeline. SCG unlocked the bridge raise by rapidly realigning both narrative and audience through a structured sprint across three work streams:

Narrative Alignment: Shifted the pitch from deep-tech engineering to a commercially compelling bridge opportunity, emphasizing de-risked traction and a defensible path to a greater than $10B exit.

Investor Targeting: Bypassed 150+ previously contacted VCs to build a fresh, highly targeted pipeline of solo angels, HNWIs, and family offices aligned with the opportunity and capable of agile, sub-six-figure check decisions.

Capital Raise Execution: Leveraged SCG's proprietary early-stage investment banking methodology and behavioral analytics to drive a minimum of three high-intent investor engagements per week throughout the sprint, generating 28 qualified prospects, 67% HNWI or family office, and accelerating the bridge round to close.

The outcome was not coincidental. It was the product of repositioning a credible opportunity in front of the right audience at the right time, with disciplined execution and SCG’s novel approach to sell-side finance for early stage opportunities at every turn of the process.